AP Statistics Curriculum 2007 Laplace

From Socr

(Created page with '===Laplace Distribution=== '''Definition''': Laplace distribution is a distribution that is symmetrical and more “peaky” than a normal distribution. The dispersion of the dat…')

Newer edit →

Revision as of 20:26, 11 July 2011

Laplace Distribution

Definition: Laplace distribution is a distribution that is symmetrical and more “peaky” than a normal distribution. The dispersion of the data around the mean is higher than that of a normal distribution. Laplace distribution is also sometimes called the double exponential distribution.

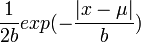

Probability density function: For X~Laplace(μ,b), the Laplace probability density function is given by

where

- e is the natural number (e = 2.71828…)

- b is a scale parameter (determines the profile of the distribution)

- μ is the mean

- x is a random variable

Cumulative density function: The Laplace cumulative distribution function is given by

![\left\{\begin{matrix}

\frac{1}{2}\exp(\frac{x-\mu}{b}) & \mbox{if }x < \mu

\\[8pt]

1-\frac{1}{2}\exp(-\frac{x-\mu}{b}) & \mbox{if }x \geq \mu

\end{matrix}\right.](/socr/uploads/math/6/b/e/6be820c4b4bb39a40b48397c84bc8617.png)

where

- e is the natural number (e = 2.71828…)

- b is a scale parameter (determines the profile of the distribution)

- μ is the mean

- x is a random variable

Moment generating function: The Laplace moment-generating function is

Expectation:

Variance: The gamma variance is

Related Distributions

- If

, then

, then

- If

, then

, then  (exponential distribution)

(exponential distribution)

Applications

The Laplace distribution is used for modeling in signal processing, various biological processes, finance, and economics. Examples of events that may be modeled by Laplace distribution include:

- Credit risk and exotic options in financial engineering

- Insurance claims

- Structural changes in switching-regime model and Kalman filter