SOCR EduMaterials Activities ApplicationsActivities StockSimulation

From Socr

(Difference between revisions)

Nchristo (Talk | contribs)

(New page: == A Model for Stock prices == * '''Description''': You can access the stock simulation applet at http://www.socr.ucla.edu/htmls/app/ . * Process for Stock Prices: Assumed a drift rate...)

Newer edit →

(New page: == A Model for Stock prices == * '''Description''': You can access the stock simulation applet at http://www.socr.ucla.edu/htmls/app/ . * Process for Stock Prices: Assumed a drift rate...)

Newer edit →

Revision as of 16:07, 3 August 2008

A Model for Stock prices

- Description: You can access the stock simulation applet at http://www.socr.ucla.edu/htmls/app/ .

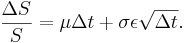

- Process for Stock Prices: Assumed a drift rate equal to μS where μ is the expected return of the stock, and variance σ2S2 where σ2 is the variance of the return of the stock. From Weiner process the model for stock prices is:

or

or

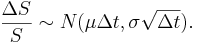

Therefore

Therefore

S Price of the stock.

ΔS Change in the stock price.

Δt Small interval of time.

ε Follows N(0,1).

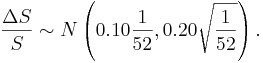

- Example: The current price of a stock is

. The expected return is μ = 0.10 per year, and the standard deviation of the return is σ = 0.20 (also per year).

. The expected return is μ = 0.10 per year, and the standard deviation of the return is σ = 0.20 (also per year).

- Find an expression for the process of the stock.

- Find the distribution of the change in

.

.

- Divide the year in weekly intervals and find the distribution of

at the end of each weekly interval.

at the end of each weekly interval.

- Therefore, sampling from this distribution we can simulate the path of the stock. The price of the stock at the end of the first interval will be S1 = S0 + ΔS1, where ΔS1 is the change during the first time interval, etc.

- Using the SOCR applet we will simulate the stock's path by dividing one year into small intervals each one of length

of a year, when

of a year, when  .

.

- The applet will select a random sample of 100 observations from N(0,1) and will compute

Suppose that ε1 = 0.58. Then

Suppose that ε1 = 0.58. Then

Therefore

ΔS1 = S0 + ΔS1 = 20 + 0.26 = 20.26.

We continue in the same fashion until we reach the end of the year.