SOCR EduMaterials Activities ApplicationsActivities StockSimulation

From Socr

A Model for Stock prices

- Description: You can access the stock simulation applet at http://www.socr.ucla.edu/htmls/app/ .

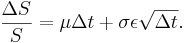

- Process for Stock Prices: Assumed a drift rate equal to μS where μ is the expected return of the stock, and variance σ2S2 where σ2 is the variance of the return of the stock. From Weiner process the model for stock prices is:

or

or

Therefore

Therefore

S Price of the stock.

ΔS Change in the stock price.

Δt Small interval of time.

ε Follows N(0,1).

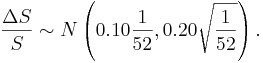

- Example: The current price of a stock is

. The expected return is μ = 0.10 per year, and the standard deviation of the return is σ = 0.20 (also per year).

. The expected return is μ = 0.10 per year, and the standard deviation of the return is σ = 0.20 (also per year).

- Find an expression for the process of the stock.

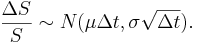

- Find the distribution of the change in S divided by S at the end of the first year. That is, find the distribution of

.

.

- Divide the year in weekly intervals and find the distribution of at the end of each weekly interval.

- Therefore, sampling from this distribution we can simulate the path of the stock. The price of the stock at the end of the first interval will be S1 = S0 + ΔS1, where ΔS1 is the change during the first time interval, etc.

- Using the SOCR applet we will simulate the stock's path by dividing one year into small intervals each one of length

of a year, when

of a year, when  , annual mean and standard deviation: μ = 0.14,σ = 0.20.

, annual mean and standard deviation: μ = 0.14,σ = 0.20.

- The applet will select a random sample of 100 observations from N(0,1) and will compute

Suppose that ε1 = 0.58. Then

Suppose that ε1 = 0.58. Then

Therefore

ΔS1 = S0 + ΔS1 = 20 + 0.26 = 20.26.

We continue in the same fashion until we reach the end of the year. Here is the SOCR applet.

- The materials above was partially taken from

Modern Portfolio Theory by Edwin J. Elton, Martin J. Gruber, Stephen J. Brown, and William N. Goetzmann, Sixth Edition, Wiley, 2003, and

Options, Futues, and Other Derivatives by John C. Hull, Sixth Edition, Pearson Prentice Hall, 2006.